About

Languages:

Explore Our Services

Preview Our Rates

Access all your mortgage options with just one application. Preview today's rates first:

Blog

Mortgage Pre-Approval in Ontario: First-Time Buyer Guide

June 15, 2026

Mortgage Pre-Approval in Ontario: What First-Time Buyers Should Know Before House Hunting

Mortgage pre-approval for Ontario buyers is not just about knowing how much a lender may approve. It is about understanding your real budget before you start looking at homes.

Your home search should start with your budget, not with the house.

That is where mortgage pre-approval comes in.

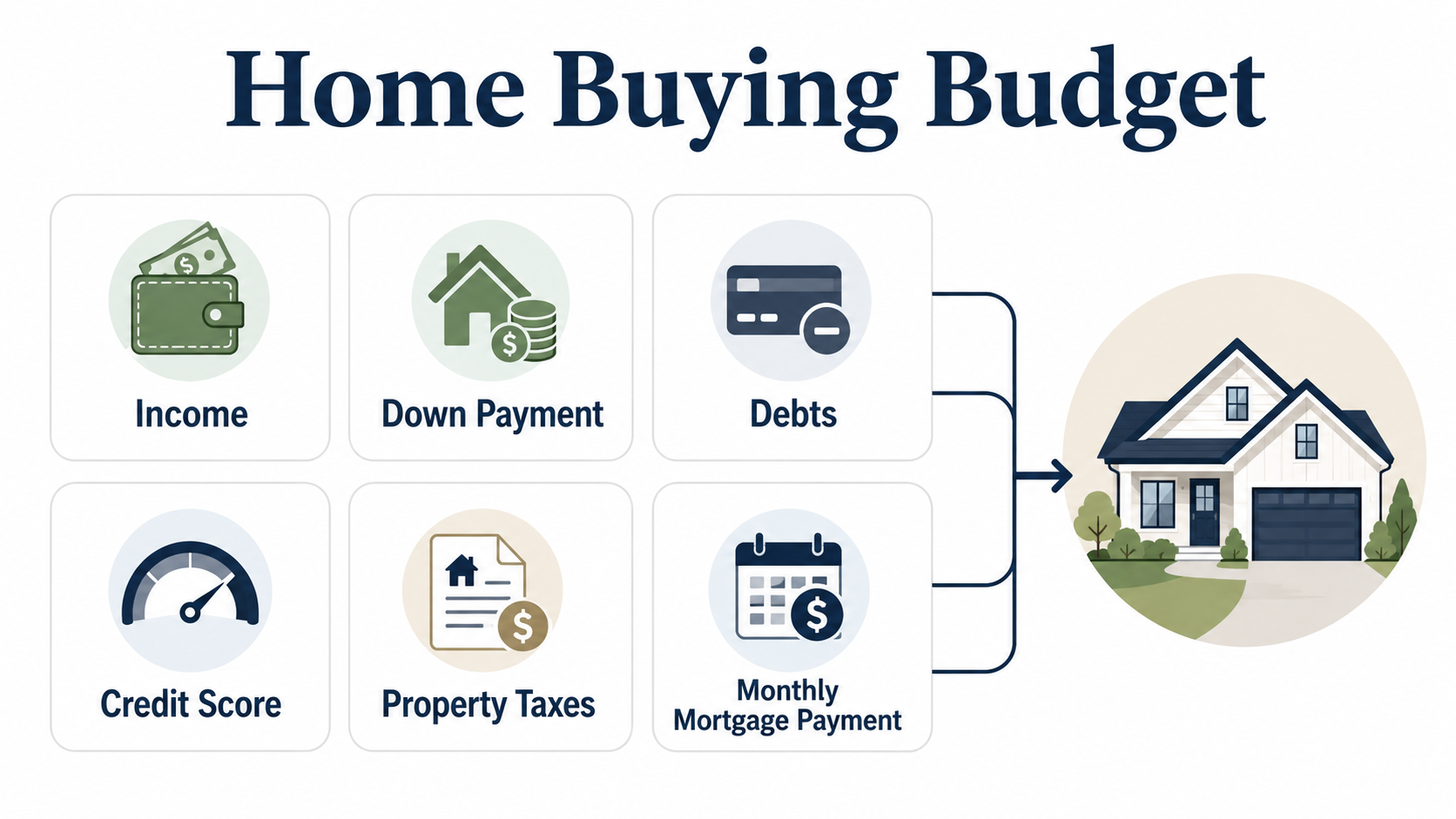

A mortgage pre-approval can help you understand how much you may be able to borrow, what your estimated payments could look like, and what price range may be more realistic for your situation. However, it is also important to understand that a pre-approval is not the same as final mortgage approval. The Government of Canada also notes that the mortgage pre-approval process does not guarantee final approval.Canada.ca

This guide explains what mortgage pre-approval means, why it matters, what documents may be needed, and what first-time buyers in Ontario should avoid before closing.

What Is a Mortgage Pre-Approval?

A mortgage pre-approval is when a lender or mortgage professional reviews your financial situation before you make an offer on a home.

They may look at things like:

- your income

- your job situation

- your down payment

- your credit history

- your existing debts

- your estimated property expenses

- your overall borrowing capacity

The goal is to estimate how much mortgage you may qualify for based on the information available at that time.

For first-time buyers, this step is useful because it gives you a clearer price range before you start looking at homes.

Why Pre-Approval Matters Before House Hunting

Many buyers start by asking:

“How much is this house?”

But the better question is:

“Can I comfortably afford this home based on my income, debts, down payment, and monthly budget?”

A pre-approval helps you avoid wasting time on homes that may not fit your real financial situation.

It can also help you:

- understand your estimated purchase budget

- know your possible monthly payment range

- identify issues early

- prepare your documents

- avoid surprises after making an offer

- shop with more confidence

CMHC recommends that buyers understand what they can afford and get mortgage pre-approval before starting their home search. CMHC recommendations

Pre-Approval Is Not Final Approval

This is one of the biggest misunderstandings among buyers.

A pre-approval does not mean the lender has fully approved the mortgage for a specific property.

Final approval usually happens after you have an accepted offer and the lender reviews the full file, including the property details.

The lender may still need to review:

- the signed purchase agreement

- MLS listing

- property type and condition

- appraisal, if required

- updated income documents

- down payment verification

- credit status

- lawyer and closing details

So even if you are pre-approved, you should avoid making major financial changes before closing.

What Documents May Be Needed for Pre-Approval?

The exact documents can vary depending on your situation, but most buyers should be ready to provide basic financial information.

Common documents may include:

Category | Examples |

|---|---|

Identification | Government-issued ID |

Income | Job letter, recent pay stubs, T4S, Notice of Assessment |

Down payment | Bank statements, investment statements, gift letter, if applicable |

Debts | Credit cards, car loans, lines of credit, student loans |

Property details | Usually needed after you make an offer |

CMHC notes that mortgage pre-approval may involve details about your job, salary, bank accounts, financial assets, loans, debts, down payment, and closing cost funds. Are you ready to buy a home?

Do Not Forget Closing Costs

Your down payment is not your only cost.

Many first-time buyers focus only on the down payment and forget that closing costs may also be needed.

Closing costs can include:

- land transfer tax

- lawyer fees

- title insurance

- appraisal fee, if required

- home inspection, if applicable

- property tax adjustments

- moving costs

CMHC notes that buyers should have sufficient funds to cover closing costs, which are often estimated at 1.5% to 4% of the purchase price.

For example, if you are buying a $600,000 home, closing costs could be a meaningful extra amount on top of your down payment.

That is why your budget should include both:

Down payment + closing costs

Not just the down payment.

Common Mistakes Buyers Make Before Pre-Approval

Here are some common mistakes first-time buyers should avoid:

1. Looking at homes before knowing their real budget

Online calculators can be helpful, but they do not replace a proper review of your income, debts, credit, and down payment.

2. Assuming pre-approval means guaranteed approval

Pre-approval is helpful, but final approval depends on the complete file and the property.

3. Forgetting about monthly comfort

Just because you may qualify for a certain amount does not mean that the payment is comfortable for your lifestyle.

4. Taking on new debt before closing

A new car loan, higher credit card balance, or new financing can affect your mortgage approval.

5. Not preparing documents early

Missing documents can slow down the process, especially when there is a financing condition deadline.

Simple Example

Let’s say a buyer wants to purchase a home in Ontario.

They have:

- stable employment income

- some savings for down payment

- one car payment

- credit card balances

- family expenses

- a target purchase price in mind

Without pre-approval, they may guess their budget based only on income.

But a lender will look at the full picture, including income, debt obligations, credit, down payment, property taxes, heating costs, condo fees if applicable, and qualifying rate.

That is why two buyers with the same income may not qualify for the same mortgage amount.

The details matter.

When Should You Get Pre-Approved?

Ideally, you should get pre-approved before you start serious house hunting.

A good time is when:

- You are planning to buy within the next few months

- You want to know your realistic price range

- You are starting to speak with a realtor

- You are comparing rent vs buying

- You want to prepare your documents early

- You want to understand whether debts or credit may affect your approval

Even if you are not ready to buy immediately, an early review can help you know what to fix or prepare.

Final Thoughts

Mortgage pre-approval is not just about impressing a realtor or seller.

It is about protecting your budget.

Before you fall in love with a home, you should know whether the numbers make sense for your income, debts, down payment, and monthly budget.

A proper pre-approval can help you shop with more confidence, avoid unrealistic expectations, and prepare for the mortgage process before making an offer.

Planning to buy your first home in Ontario?

Before you start house hunting, it is better to understand your real affordability.

You can contact me to review your mortgage options and prepare for the buying process.

Amandeep Singh Bhatia

Mortgage Agent Level 1

Mob: +1 647-229-9477

Email: asbhatia@akal.ca

AKAL Mortgages Inc.

Lic #10845

Independently owned and operated.

Stay Connected

Subscribe to our Newsletter and you'll stay up to date on rates that help you save thousands in interest.